Non-linear Modeling

weiya

5/8/2021

本文基于 ISLR 的 7.8 节。

首先加载必要的包,

library(ISLR)其中包括本文需要处理的数据 Wage,这是中大西洋地区(Mid-Atlantic) 3000 个男性工作者的工资及其它数据。

str(Wage)## 'data.frame': 3000 obs. of 11 variables:

## $ year : int 2006 2004 2003 2003 2005 2008 2009 2008 2006 2004 ...

## $ age : int 18 24 45 43 50 54 44 30 41 52 ...

## $ maritl : Factor w/ 5 levels "1. Never Married",..: 1 1 2 2 4 2 2 1 1 2 ...

## $ race : Factor w/ 4 levels "1. White","2. Black",..: 1 1 1 3 1 1 4 3 2 1 ...

## $ education : Factor w/ 5 levels "1. < HS Grad",..: 1 4 3 4 2 4 3 3 3 2 ...

## $ region : Factor w/ 9 levels "1. New England",..: 2 2 2 2 2 2 2 2 2 2 ...

## $ jobclass : Factor w/ 2 levels "1. Industrial",..: 1 2 1 2 2 2 1 2 2 2 ...

## $ health : Factor w/ 2 levels "1. <=Good","2. >=Very Good": 1 2 1 2 1 2 2 1 2 2 ...

## $ health_ins: Factor w/ 2 levels "1. Yes","2. No": 2 2 1 1 1 1 1 1 1 1 ...

## $ logwage : num 4.32 4.26 4.88 5.04 4.32 ...

## $ wage : num 75 70.5 131 154.7 75 ...为了方便引用,暴露数据框的列名,

attach(Wage)## The following object is masked from Auto:

##

## year## The following objects are masked from Wage (pos = 6):

##

## age, education, health, health_ins, jobclass, logwage, maritl,

## race, region, wage, year多项式样条

首先我们用多项式样条进行拟合工资 wage 和年龄 age 之间的关系,

fit = lm(wage ~ poly(age, 4), data = Wage)

coef(summary(fit))## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 111.70361 0.7287409 153.283015 0.000000e+00

## poly(age, 4)1 447.06785 39.9147851 11.200558 1.484604e-28

## poly(age, 4)2 -478.31581 39.9147851 -11.983424 2.355831e-32

## poly(age, 4)3 125.52169 39.9147851 3.144742 1.678622e-03

## poly(age, 4)4 -77.91118 39.9147851 -1.951938 5.103865e-02其中 poly(age, 4) 返回的是正交化的多项式,即每一列是 age^i, i=1,2,3,4 的线性组合。如果我们想直接用 age^i,

fit2 = lm(wage ~ poly(age, 4, raw = T), data = Wage)

coef(summary(fit2))## Estimate Std. Error t value Pr(>|t|)

## (Intercept) -1.841542e+02 6.004038e+01 -3.067172 0.0021802539

## poly(age, 4, raw = T)1 2.124552e+01 5.886748e+00 3.609042 0.0003123618

## poly(age, 4, raw = T)2 -5.638593e-01 2.061083e-01 -2.735743 0.0062606446

## poly(age, 4, raw = T)3 6.810688e-03 3.065931e-03 2.221409 0.0263977518

## poly(age, 4, raw = T)4 -3.203830e-05 1.641359e-05 -1.951938 0.0510386498这等价于

fit2a = lm(wage ~ age + I(age^2) + I(age^3) + I(age^4), data = Wage)

summary(fit2a)##

## Call:

## lm(formula = wage ~ age + I(age^2) + I(age^3) + I(age^4), data = Wage)

##

## Residuals:

## Min 1Q Median 3Q Max

## -98.707 -24.626 -4.993 15.217 203.693

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) -1.842e+02 6.004e+01 -3.067 0.002180 **

## age 2.125e+01 5.887e+00 3.609 0.000312 ***

## I(age^2) -5.639e-01 2.061e-01 -2.736 0.006261 **

## I(age^3) 6.811e-03 3.066e-03 2.221 0.026398 *

## I(age^4) -3.204e-05 1.641e-05 -1.952 0.051039 .

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 39.91 on 2995 degrees of freedom

## Multiple R-squared: 0.08626, Adjusted R-squared: 0.08504

## F-statistic: 70.69 on 4 and 2995 DF, p-value: < 2.2e-16而不加 -I(),

fit2a.wrong = lm(wage ~ age + age^2 + age^3 + age^4, data = Wage)

summary(fit2a.wrong)##

## Call:

## lm(formula = wage ~ age + age^2 + age^3 + age^4, data = Wage)

##

## Residuals:

## Min 1Q Median 3Q Max

## -100.265 -25.115 -6.063 16.601 205.748

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 81.70474 2.84624 28.71 <2e-16 ***

## age 0.70728 0.06475 10.92 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 40.93 on 2998 degrees of freedom

## Multiple R-squared: 0.03827, Adjusted R-squared: 0.03795

## F-statistic: 119.3 on 1 and 2998 DF, p-value: < 2.2e-16其结果等价于直接去掉高阶项,

fit2a.wrong2 = lm(wage ~ age, data = Wage)

summary(fit2a.wrong2)##

## Call:

## lm(formula = wage ~ age, data = Wage)

##

## Residuals:

## Min 1Q Median 3Q Max

## -100.265 -25.115 -6.063 16.601 205.748

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 81.70474 2.84624 28.71 <2e-16 ***

## age 0.70728 0.06475 10.92 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 40.93 on 2998 degrees of freedom

## Multiple R-squared: 0.03827, Adjusted R-squared: 0.03795

## F-statistic: 119.3 on 1 and 2998 DF, p-value: < 2.2e-16更多解释详见 ?formula.

除此之外,我们也可以用

fit2b = lm(wage ~ cbind(age, age^2, age^3, age^4), data = Wage)

summary(fit2b)##

## Call:

## lm(formula = wage ~ cbind(age, age^2, age^3, age^4), data = Wage)

##

## Residuals:

## Min 1Q Median 3Q Max

## -98.707 -24.626 -4.993 15.217 203.693

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) -1.842e+02 6.004e+01 -3.067 0.002180

## cbind(age, age^2, age^3, age^4)age 2.125e+01 5.887e+00 3.609 0.000312

## cbind(age, age^2, age^3, age^4) -5.639e-01 2.061e-01 -2.736 0.006261

## cbind(age, age^2, age^3, age^4) 6.811e-03 3.066e-03 2.221 0.026398

## cbind(age, age^2, age^3, age^4) -3.204e-05 1.641e-05 -1.952 0.051039

##

## (Intercept) **

## cbind(age, age^2, age^3, age^4)age ***

## cbind(age, age^2, age^3, age^4) **

## cbind(age, age^2, age^3, age^4) *

## cbind(age, age^2, age^3, age^4) .

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 39.91 on 2995 degrees of freedom

## Multiple R-squared: 0.08626, Adjusted R-squared: 0.08504

## F-statistic: 70.69 on 4 and 2995 DF, p-value: < 2.2e-16拟合好模型后,我们可以进行预测,

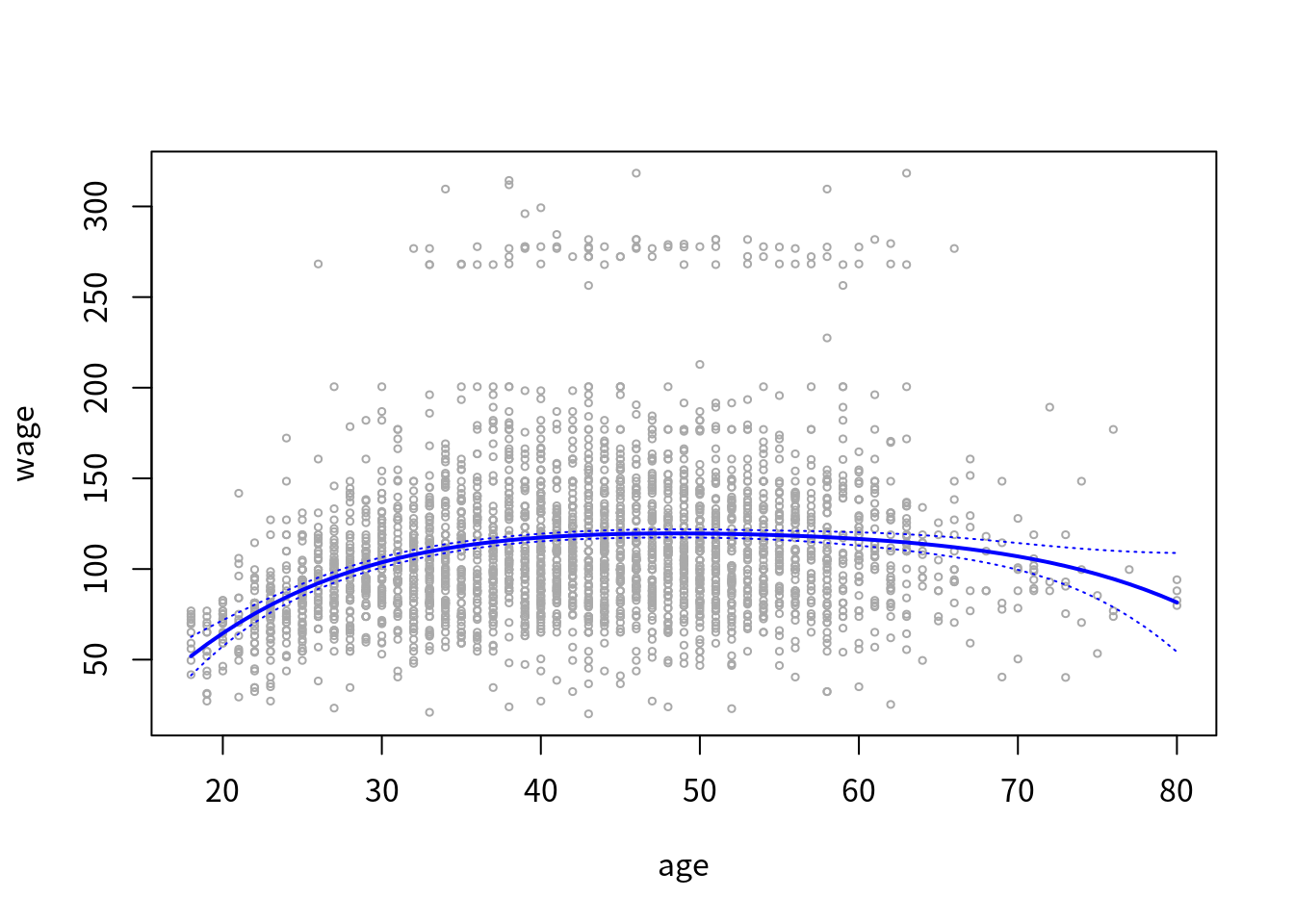

agelims = range(age)

age.grid = seq(from = agelims[1], to = agelims[2])

preds = predict(fit, newdata = list(age = age.grid), se = TRUE)

se.bands = cbind(preds$fit + 2*preds$se.fit, preds$fit - 2*preds$se.fit)并且画出图象,

# mar = (bottom, left, top, right) specifies the margin

# oma specifies the outer margin

# par(mfrow = c(1, 2), mar = c(4.5, 4.5, 1, 1), oma = c(0, 0, 4, 0))

# cex specifies the amount by which plotting text and symbols should be magnified relative to the default

# it has four sub-arguments: cex.axis, cex.lab, cex.main, cex.sub

plot(age, wage, xlim = agelims, cex=.5, col = "darkgrey")

# title("Degree 4 Polynomial", outer = T)

lines(age.grid, preds$fit, lwd = 2, col = "blue")

matlines(age.grid, se.bands, lwd = 1, col = "blue", lty=3)

基函数进行正交化与否对预测结果无影响,

preds2 = predict(fit2, newdata = list(age = age.grid), se = TRUE)

max(abs(preds$fit - preds2$fit))## [1] 1.641354e-12多项式回归的阶数通常通过假设检验

- \(H_0\): \(\cM_1\) 能充分地解释数据

- \(H_1\): 需要更复杂的模型 \(\cM_2\)

进行确定。为了应用 ANOVA,其中 \(\cM_1 \subset \cM_2\) 要求是 nested。 基本思想是,同时拟合 \(\cM_i,i=1,2\),然后检验更复杂的模型是否显著地比简单的模型更好。这其实也可以看成是线性回归中同时检验多个参数的显著性,如 ESL 中 (3.13) 式所示

fit.1 = lm(wage ~ age, data = Wage)

fit.2 = lm(wage ~ poly(age, 2), data = Wage)

fit.3 = lm(wage ~ poly(age, 3), data = Wage)

fit.4 = lm(wage ~ poly(age, 4), data = Wage)

fit.5 = lm(wage ~ poly(age, 5), data = Wage)

anova(fit.1, fit.2, fit.3, fit.4, fit.5)## Analysis of Variance Table

##

## Model 1: wage ~ age

## Model 2: wage ~ poly(age, 2)

## Model 3: wage ~ poly(age, 3)

## Model 4: wage ~ poly(age, 4)

## Model 5: wage ~ poly(age, 5)

## Res.Df RSS Df Sum of Sq F Pr(>F)

## 1 2998 5022216

## 2 2997 4793430 1 228786 143.5931 < 2.2e-16 ***

## 3 2996 4777674 1 15756 9.8888 0.001679 **

## 4 2995 4771604 1 6070 3.8098 0.051046 .

## 5 2994 4770322 1 1283 0.8050 0.369682

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1结果表明,\(\cM_1,\cM_2\) 不够(\(p\)值远小于 0.5),而 \(\cM_3,\cM_4\) 差不多(\(p\)值约等于0.5),而 \(\cM_5\) 则不必要(\(p\)值远大于 0.5)。

另外,因为 \(\cM_4\) 与 \(\cM_5\) 只差一项,换句话说,可以看成是检验 \(\cM_5\) 中那一项的系数是否为零,所以上述的 \(p\) 值与下面对 age^5 这一项的系数进行 \(t\) 检验的 \(p\) 值相等,

coef(summary(fit.5))## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 111.70361 0.7287647 153.2780243 0.000000e+00

## poly(age, 5)1 447.06785 39.9160847 11.2001930 1.491111e-28

## poly(age, 5)2 -478.31581 39.9160847 -11.9830341 2.367734e-32

## poly(age, 5)3 125.52169 39.9160847 3.1446392 1.679213e-03

## poly(age, 5)4 -77.91118 39.9160847 -1.9518743 5.104623e-02

## poly(age, 5)5 -35.81289 39.9160847 -0.8972045 3.696820e-01另外,根据 \(F\) 分布与 \(t\) 分布直接的关系,

如果 \(X\sim t_n\),则 \(X^2 \sim F(1, n)\),且 \(X^{-2}\sim F(n,1)\)。

可以发现两者统计量存在平方关系。

注意到,除了 age^5 这一项的 \(p\) 值相等,其它项的 \(p\) 值也能大致与上述对应上去,这里应该(TODO)是跟正交化有关。一般而言,ANOVA 适用场景更广,比如

fit.1 = lm(wage ~ education + age, data = Wage)

fit.2 = lm(wage ~ education + poly(age, 2), data = Wage)

fit.3 = lm(wage ~ education + poly(age, 3), data = Wage)

anova(fit.1, fit.2, fit.3)## Analysis of Variance Table

##

## Model 1: wage ~ education + age

## Model 2: wage ~ education + poly(age, 2)

## Model 3: wage ~ education + poly(age, 3)

## Res.Df RSS Df Sum of Sq F Pr(>F)

## 1 2994 3867992

## 2 2993 3725395 1 142597 114.6969 <2e-16 ***

## 3 2992 3719809 1 5587 4.4936 0.0341 *

## ---

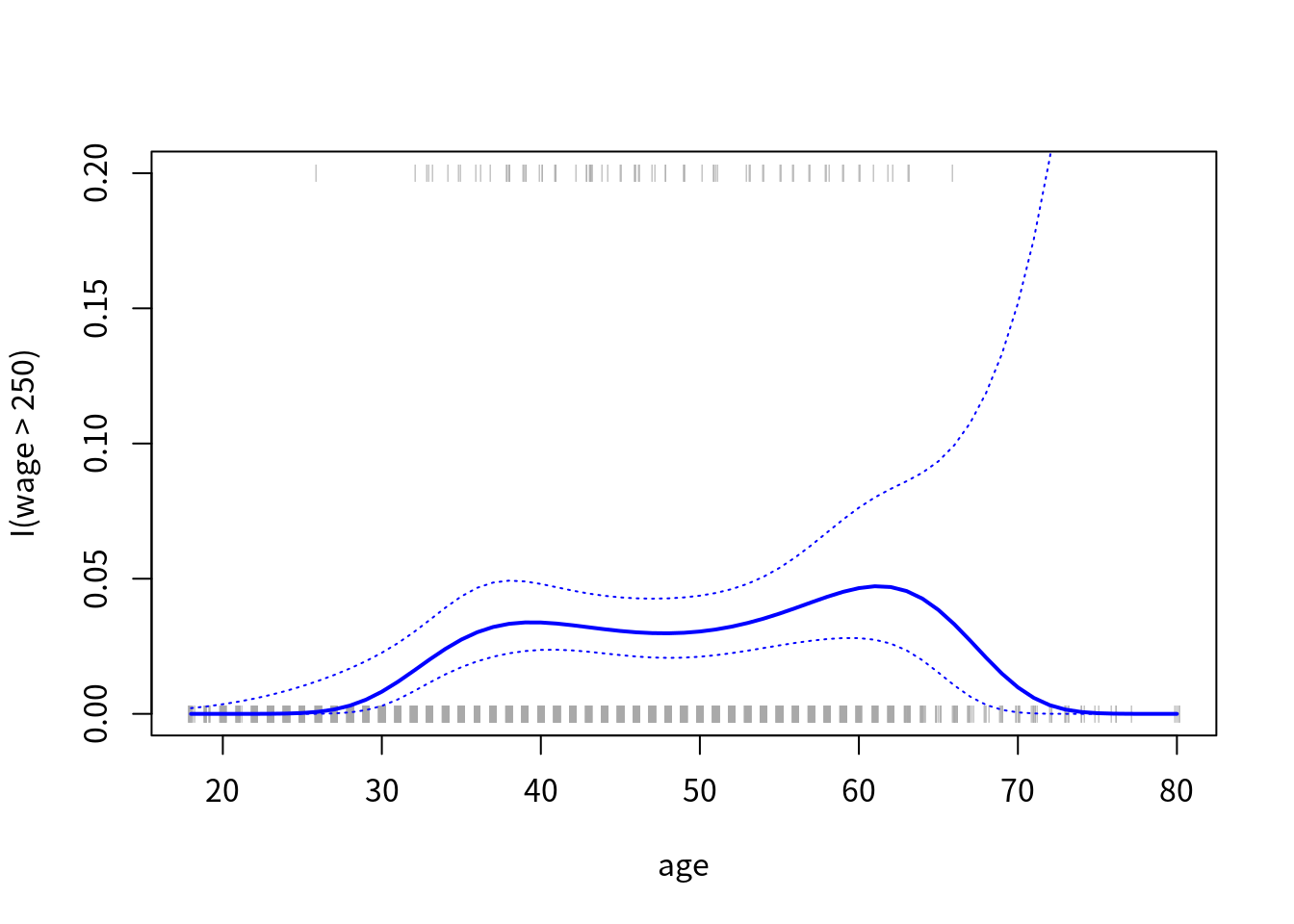

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1下一步我们想预测某个工人其是否每年赚够 $250,000,此时变成了二值变量,

fit = glm(I(wage > 250) ~ poly(age, 4), data = Wage, family = binomial)

preds = predict(fit, newdata = list(age = age.grid), se = T)

pfit = exp(preds$fit) / (1 + exp(preds$fit))

se.bands.logit = cbind(preds$fit + 2*preds$se.fit, preds$fit - 2*preds$se.fit)

se.bands = exp(se.bands.logit) / (1 + exp(se.bands.logit))一种不太恰当的计算方法为

preds = predict(fit, newdata = list(age = age.grid), type = "response", se = T)其结果可能为负,而概率不可能小于 0。

作出如下图象,其中 rug plot 将少于 250k 收入的人放在了 \(y=0\) 上,而大于 250k 收入的人放在了 \(y=0.2\) 上。

plot(age, I(wage>250), xlim = agelims, type = "n", ylim = c(0, 0.2))

points(jitter(age), I((wage>250)/5), cex = 0.5, pch = "|", col = "darkgrey")

lines(age.grid, pfit, lwd = 2, col = "blue")

matlines(age.grid, se.bands, lwd = 1, col = "blue", lty=3)

阶梯函数

在 \(X\) 的定义域内选择 \(K\) 个分隔点,\(c_i,i=1,\ldots,K\),定义

\[\begin{align*} C_0(X) & = I(X < c_1)\\ C_1(X) &= I(c_1 \le X < c_2)\\ &\vdots\\ C_{K-1}(X) &=I(c_{K-1}\le X < c_K)\\ C_K(X) &= I(c_K \le X) \end{align*}\]

然后通过最小二乘拟合

\[ y_i = \beta_0 + \beta_1C_1(x_i) +\cdots \beta_KC_K(x_i) + \epsilon_i\,, \]

其中 \(\beta_0\) 可以解释成 \(X<c_1\) 时响应变量的均值,而 \(\beta_j\) 为相较于 \(X < c_1\),在 \(c_j\le X < c_{j+1}\) 范围的响应变量的均值的增加。首先我们取定分隔点,

table(cut(age, 4))##

## (17.9,33.5] (33.5,49] (49,64.5] (64.5,80.1]

## 750 1399 779 72然后应用线性回归,

fit = lm(wage ~ cut(age, 4), data = Wage)

coef(summary(fit))## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 94.158392 1.476069 63.789970 0.000000e+00

## cut(age, 4)(33.5,49] 24.053491 1.829431 13.148074 1.982315e-38

## cut(age, 4)(49,64.5] 23.664559 2.067958 11.443444 1.040750e-29

## cut(age, 4)(64.5,80.1] 7.640592 4.987424 1.531972 1.256350e-01样条

采用回归样条,

library(splines)

fit = lm(wage ~ bs(age, knots = c(25, 40, 60)), data = Wage)

pred = predict(fit, newdata = list(age = age.grid), se = T)

plot(age, wage, col = "gray")

lines(age.grid, pred$fit, lwd = 2)

lines(age.grid, pred$fit+2*pred$se, lty = "dashed")

lines(age.grid, pred$fit-2*pred$se, lty = "dashed")

fit = lm(wage ~ I(bs(age, knots = c(25, 40, 60))), data = Wage)

pred = predict(fit, newdata = list(age = age.grid), se = T)注意此处 formula 中加不加 I() 都能正确地处理。默认 bs() 是不包含截距的,而将其置于回归函数中,若强制 bs(intercept=TRUE),则回归时应用

fit = lm(wage ~ 0 + bs(age, knots = c(25, 40, 60), intercept = TRUE), data = Wage)另见 笔记:B spline in R, C++ and Python

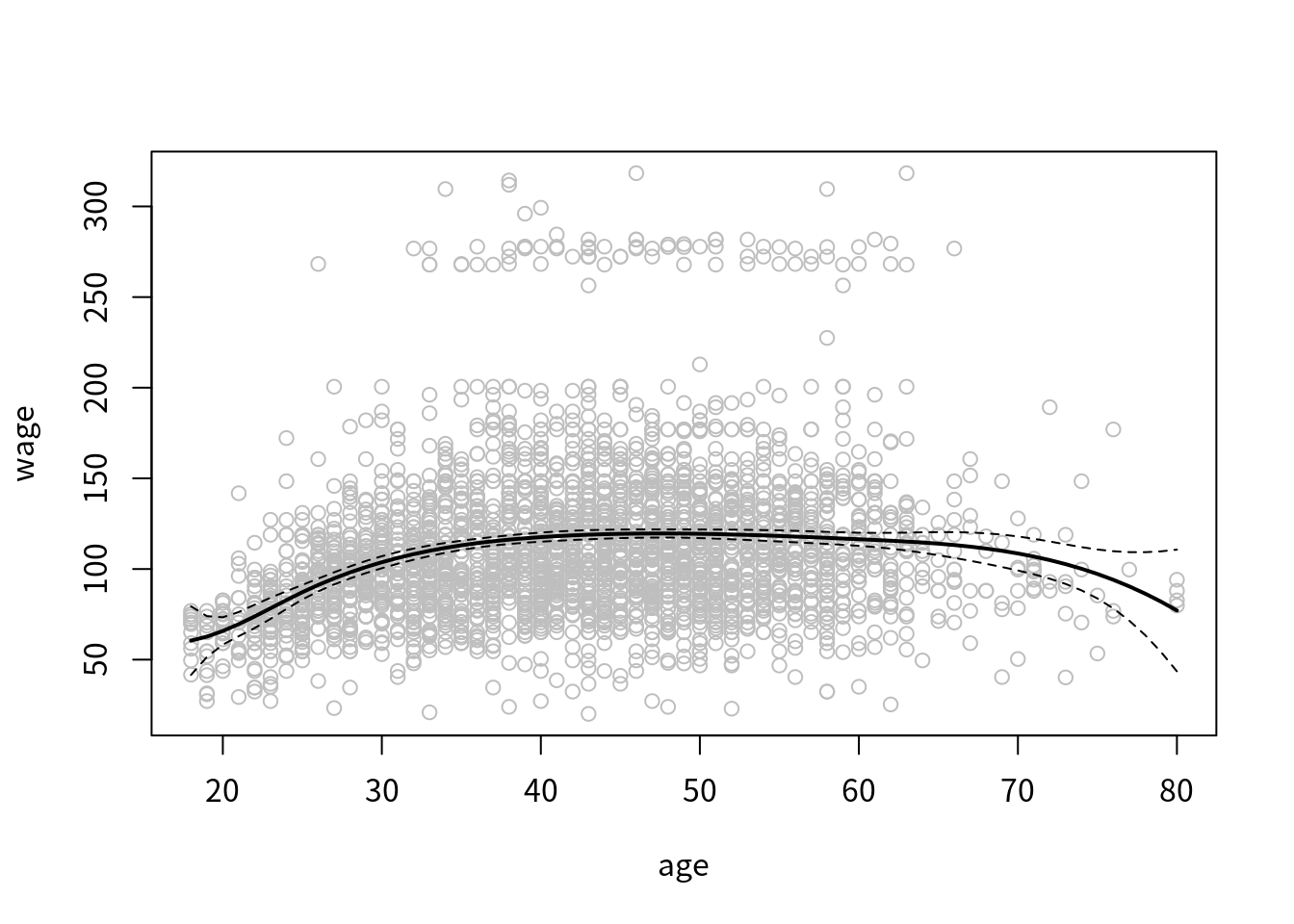

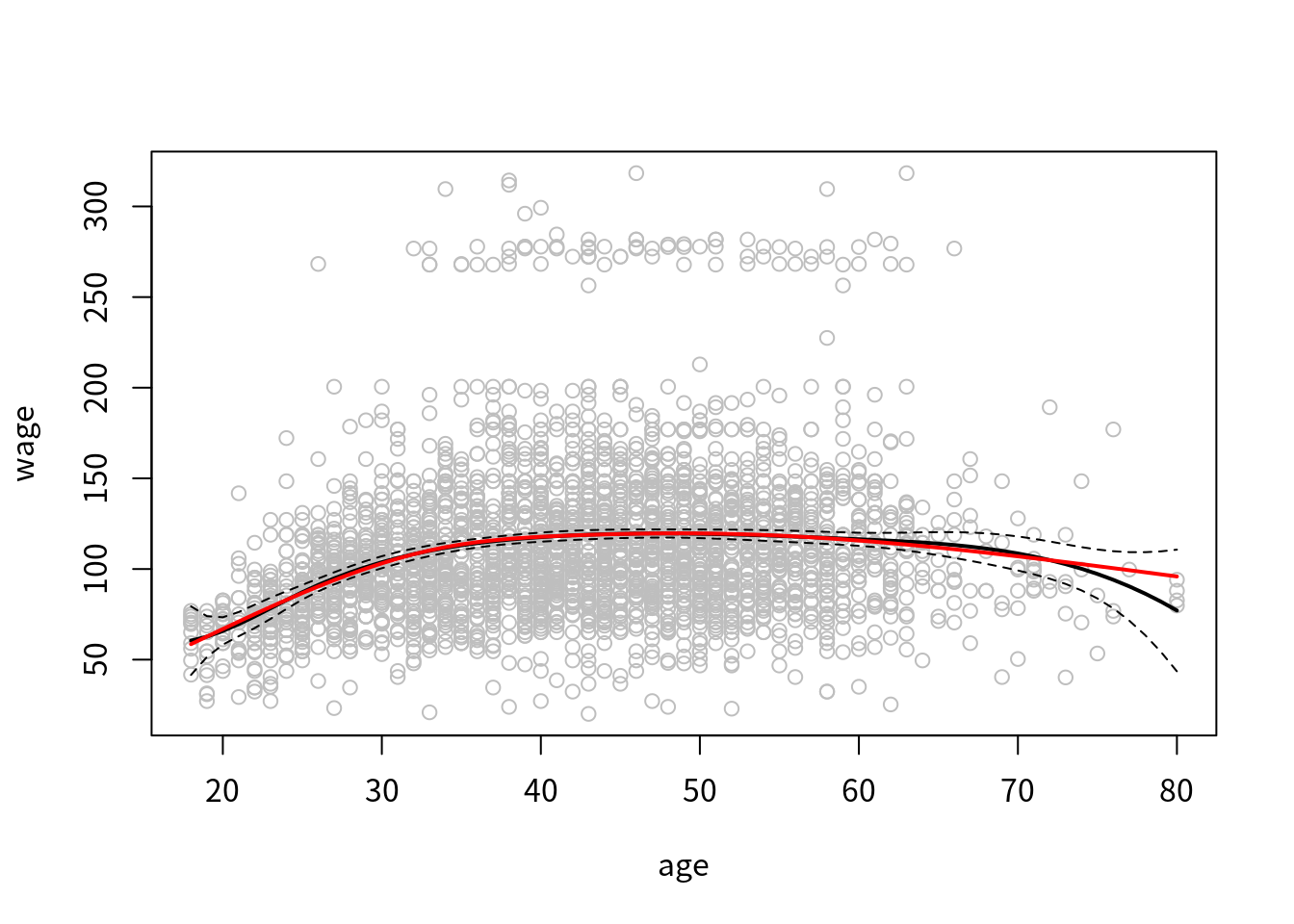

我们也可以用自然样条,

pred = predict(fit, newdata = list(age = age.grid), se = T)

plot(age, wage, col = "gray")

lines(age.grid, pred$fit, lwd = 2)

lines(age.grid, pred$fit+2*pred$se, lty = "dashed")

lines(age.grid, pred$fit-2*pred$se, lty = "dashed")

fit2 = lm(wage ~ ns(age, df=4), data = Wage)

pred2 = predict(fit2, newdata = list(age = age.grid), se = T)

lines(age.grid, pred2$fit, col = "red", lwd = 2)

事实上,ns() 也是由 B-splines 计算得到的,详见 Issue 235: Ex. derive natural spline bases from B-spline bases

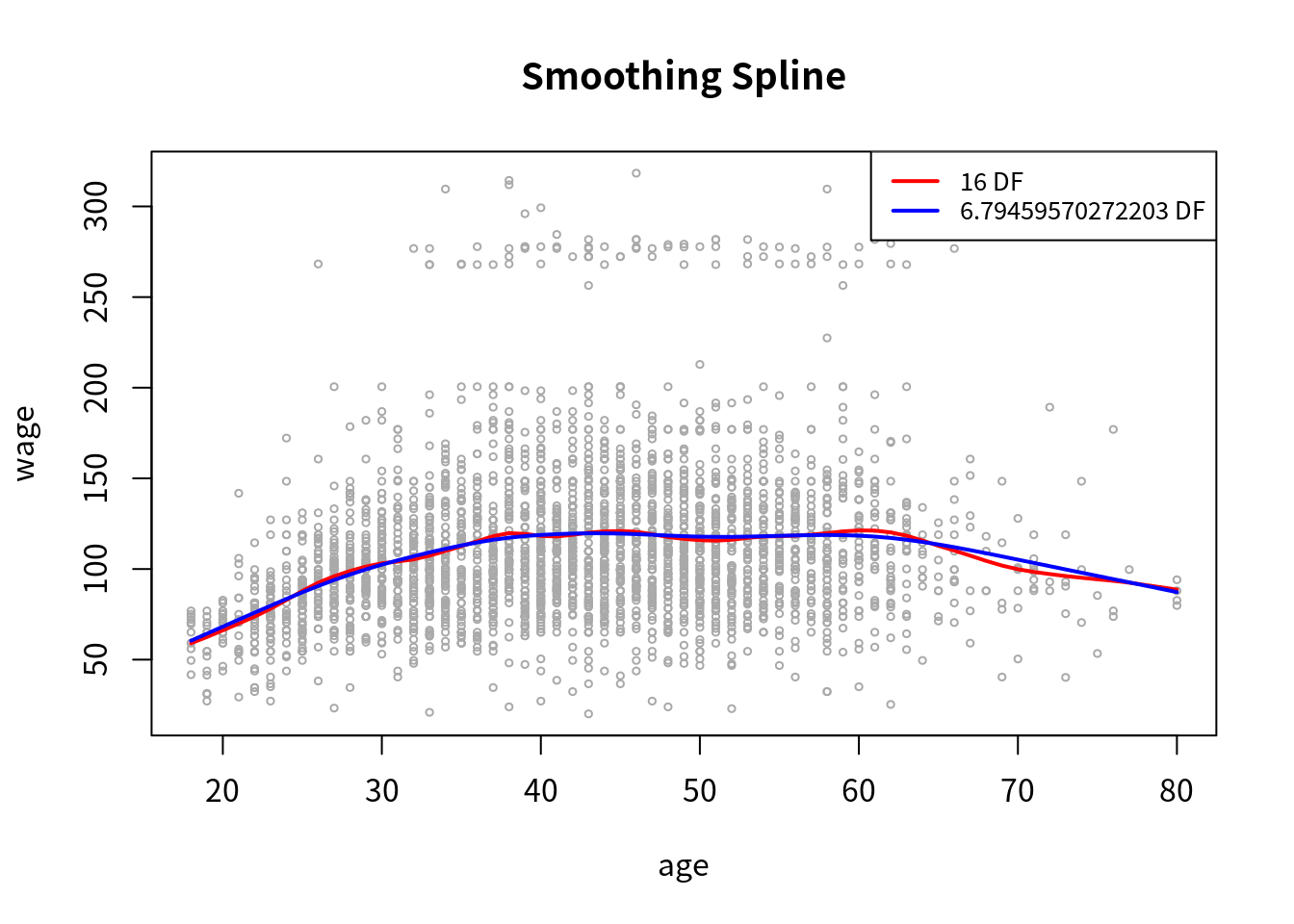

为了拟合光滑样条,我们可以用

plot(age, wage, xlim = agelims, cex = .5, col = "darkgrey")

title("Smoothing Spline")

fit = smooth.spline(age, wage, df = 16)

fit2 = smooth.spline(age, wage, cv=TRUE)## Warning in smooth.spline(age, wage, cv = TRUE): cross-validation with non-

## unique 'x' values seems doubtfullines(fit, col="red", lwd=2)

lines(fit2, col="blue", lwd=2)

legend("topright", legend = c("16 DF", paste0(fit2$df, " DF")),

col = c("red", "blue"), lty = 1, lwd = 2, cex = 0.8)

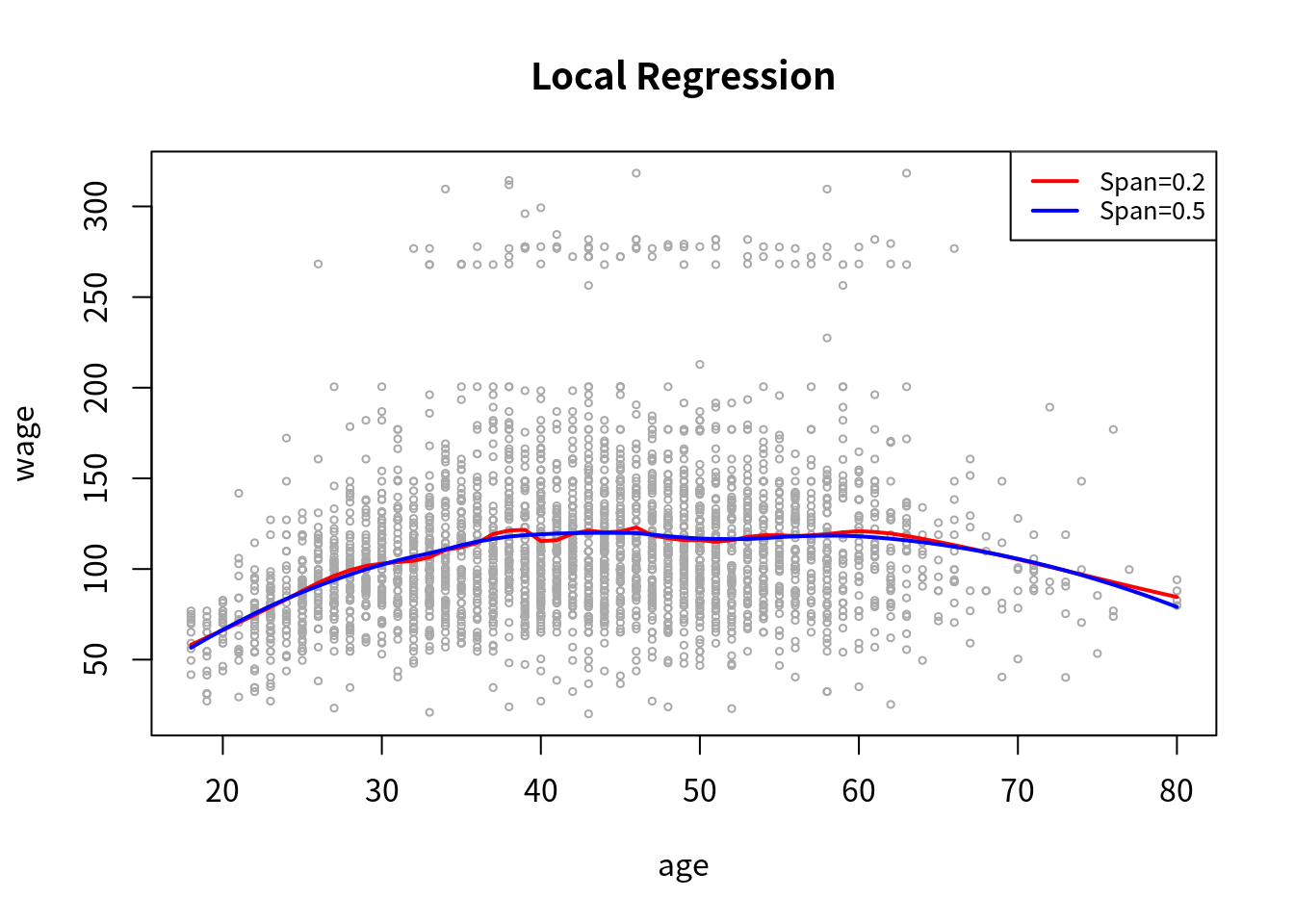

局部回归可以通过下列代码实现,

plot(age, wage, xlim = agelims, cex = .5, col = "darkgrey")

title("Local Regression")

# each neighborhood consists of 20% of the observations

fit = loess(wage ~ age, span = 0.2, data = Wage)

fit2 = loess(wage ~ age, span = 0.5, data = Wage)

lines(age.grid, predict(fit, data.frame(age = age.grid)), col = "red", lwd = 2)

lines(age.grid, predict(fit2, data.frame(age = age.grid)), col = "blue", lwd = 2)

legend("topright", legend = c("Span=0.2", "Span=0.5"),

col = c("red", "blue"), lty = 1, lwd = 2, cex = 0.8)

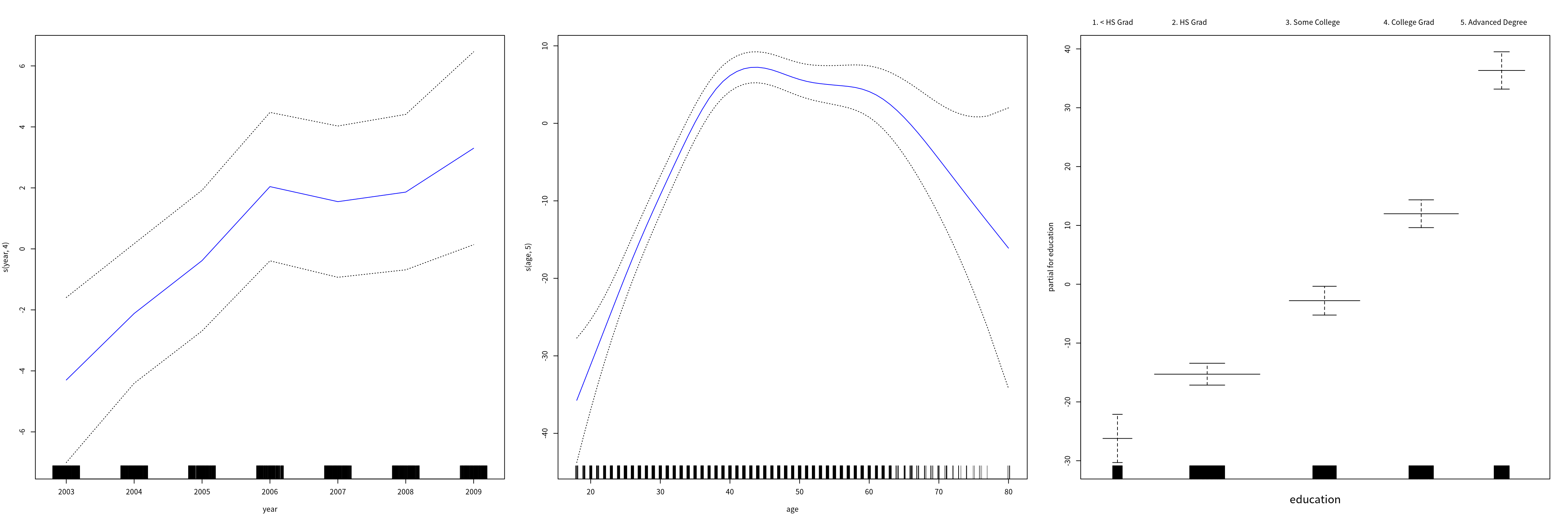

广义可加模型

首先可以用普通线性回归来构建,

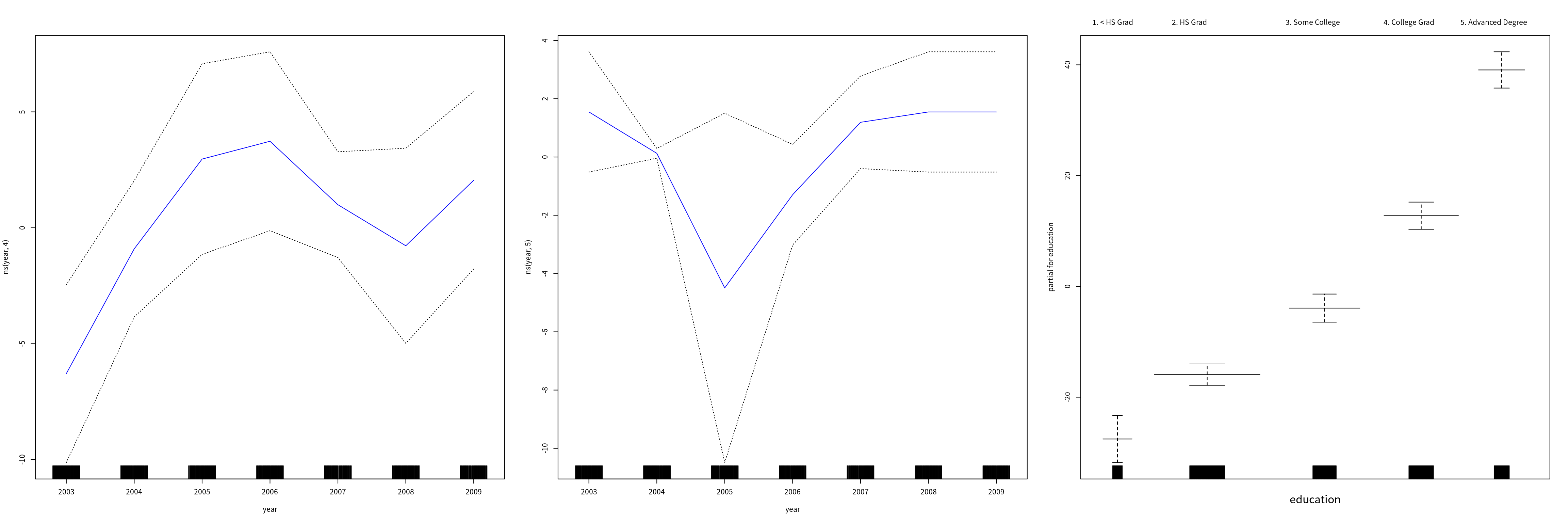

gam1 = lm(wage ~ ns(year, 4) + ns(year, 5) + education, data = Wage)为了使用光滑样条,采用 gam 包,

library(gam)

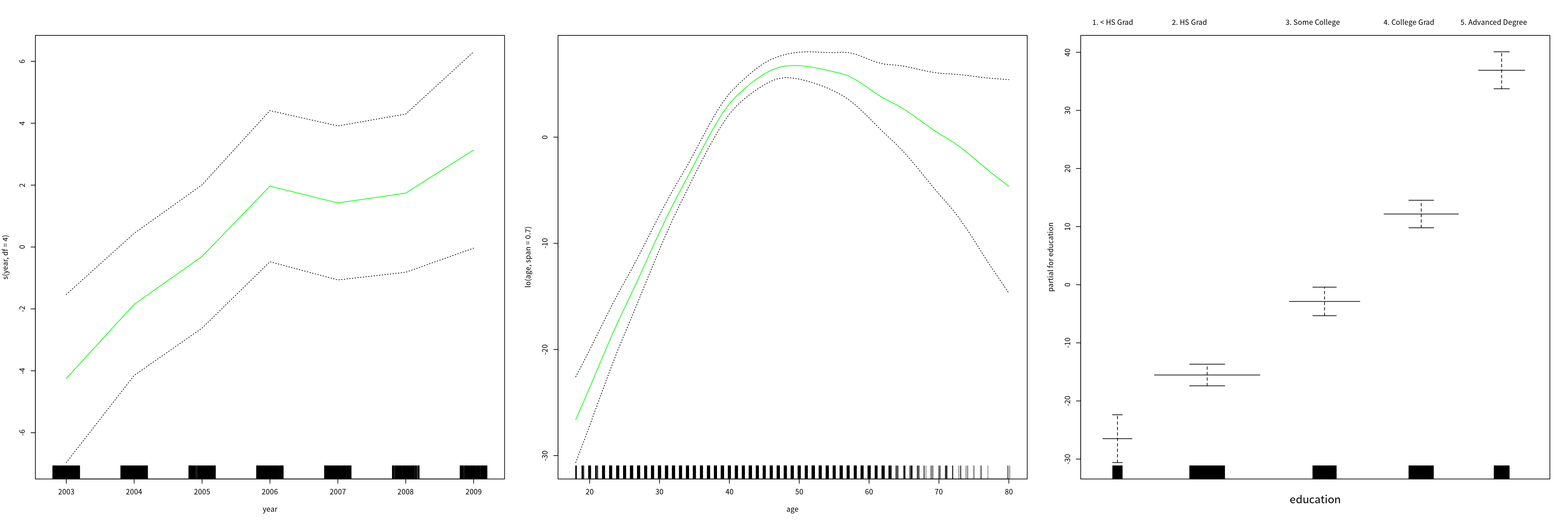

gam.m3 = gam(wage ~ s(year, 4) + s(age, 5) + education, data = Wage)

par(mfrow = c(1, 3))

plot(gam.m3, se = TRUE, col = "blue", cex = 4)

因为 gam.m3 是 gam 类的一个实例,则 plot() 实际调用了 plot.gam(),我们也可以对 gam1 画图,

par(mfrow = c(1, 3))

plot.Gam(gam1, se = TRUE, col = "blue")

这些图中关于 year 的函数看起来都像是线性,为此考虑以下几种模型

- \(\cM_1\): 不包含

year的 GAM - \(\cM_2\): 采用关于

year为线性函数的 GAM - \(\cM_3\): 采用关于

year为样条函数的 GAM

gam.m1 = gam(wage ~ s(age, 5) + education, data = Wage)

gam.m2 = gam(wage ~ year + s(age, 5) + education, data = Wage)

anova(gam.m1, gam.m2, gam.m3, test = "F")## Analysis of Deviance Table

##

## Model 1: wage ~ s(age, 5) + education

## Model 2: wage ~ year + s(age, 5) + education

## Model 3: wage ~ s(year, 4) + s(age, 5) + education

## Resid. Df Resid. Dev Df Deviance F Pr(>F)

## 1 2990 3711731

## 2 2989 3693842 1 17889.2 14.4771 0.0001447 ***

## 3 2986 3689770 3 4071.1 1.0982 0.3485661

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1由结果可以看出,\(\cM_2\) 优于 \(\cM_1\),但是没有充足采用 \(\cM_3\),于是我们采用 \(\cM_2\),

summary(gam.m2)##

## Call: gam(formula = wage ~ year + s(age, 5) + education, data = Wage)

## Deviance Residuals:

## Min 1Q Median 3Q Max

## -119.959 -19.647 -3.199 13.969 213.562

##

## (Dispersion Parameter for gaussian family taken to be 1235.812)

##

## Null Deviance: 5222086 on 2999 degrees of freedom

## Residual Deviance: 3693842 on 2989 degrees of freedom

## AIC: 29885.06

##

## Number of Local Scoring Iterations: NA

##

## Anova for Parametric Effects

## Df Sum Sq Mean Sq F value Pr(>F)

## year 1 27154 27154 21.973 2.89e-06 ***

## s(age, 5) 1 194535 194535 157.415 < 2.2e-16 ***

## education 4 1069081 267270 216.271 < 2.2e-16 ***

## Residuals 2989 3693842 1236

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Anova for Nonparametric Effects

## Npar Df Npar F Pr(F)

## (Intercept)

## year

## s(age, 5) 4 32.46 < 2.2e-16 ***

## education

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1preds = predict(gam.m2, newdata = Wage)除了使用光滑样条,我们还可以用局部回归,

gam.lo = gam(wage ~ s(year, df = 4) + lo(age, span = 0.7) + education, data = Wage)

par(mfrow = c(1, 3))

plot(gam.lo, se = T, col = "green")

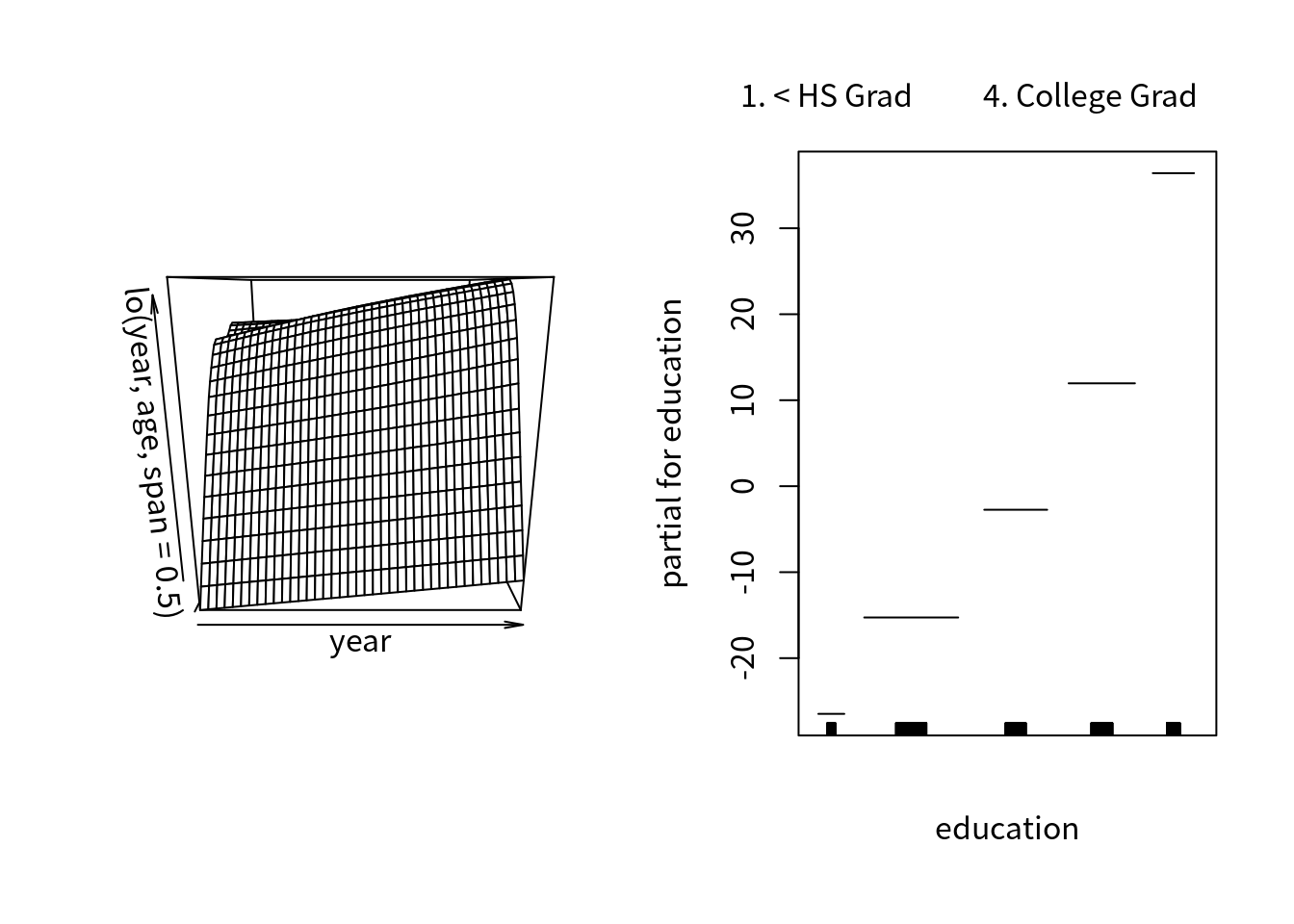

而且可以使用交叉项,

gam.lo.i = gam(wage ~ lo(year, age, span = 0.5) + education, data = Wage)## Warning in lo.wam(x, z, wz, fit$smooth, which, fit$smooth.frame,

## bf.maxit, : liv too small. (Discovered by lowesd)## Warning in lo.wam(x, z, wz, fit$smooth, which, fit$smooth.frame,

## bf.maxit, : lv too small. (Discovered by lowesd)## Warning in lo.wam(x, z, wz, fit$smooth, which, fit$smooth.frame,

## bf.maxit, : liv too small. (Discovered by lowesd)## Warning in lo.wam(x, z, wz, fit$smooth, which, fit$smooth.frame,

## bf.maxit, : lv too small. (Discovered by lowesd)以下代码可以画出交叉项的二维平面

library(akima)

par(mfrow = c(1, 2))

plot(gam.lo.i)

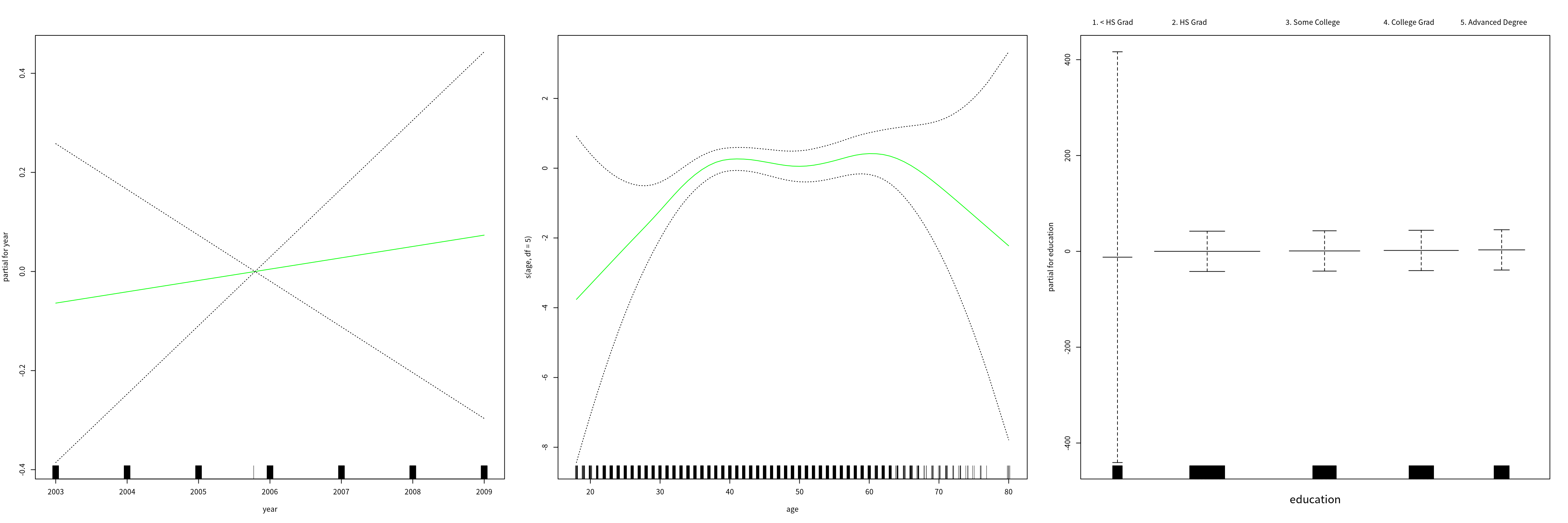

类似地,通过 I() 可以对二值变量应用 logistic GAM,

gam.lr = gam(I(wage > 250) ~ year + s(age, df = 5) + education, family = binomial, data = Wage)

par(mfrow = c(1, 3))

plot(gam.lr, se = T, col = "green")

容易观察到在 <HS 类别中没有高收入者,

table(education, I(wage > 250))##

## education FALSE TRUE

## 1. < HS Grad 268 0

## 2. HS Grad 966 5

## 3. Some College 643 7

## 4. College Grad 663 22

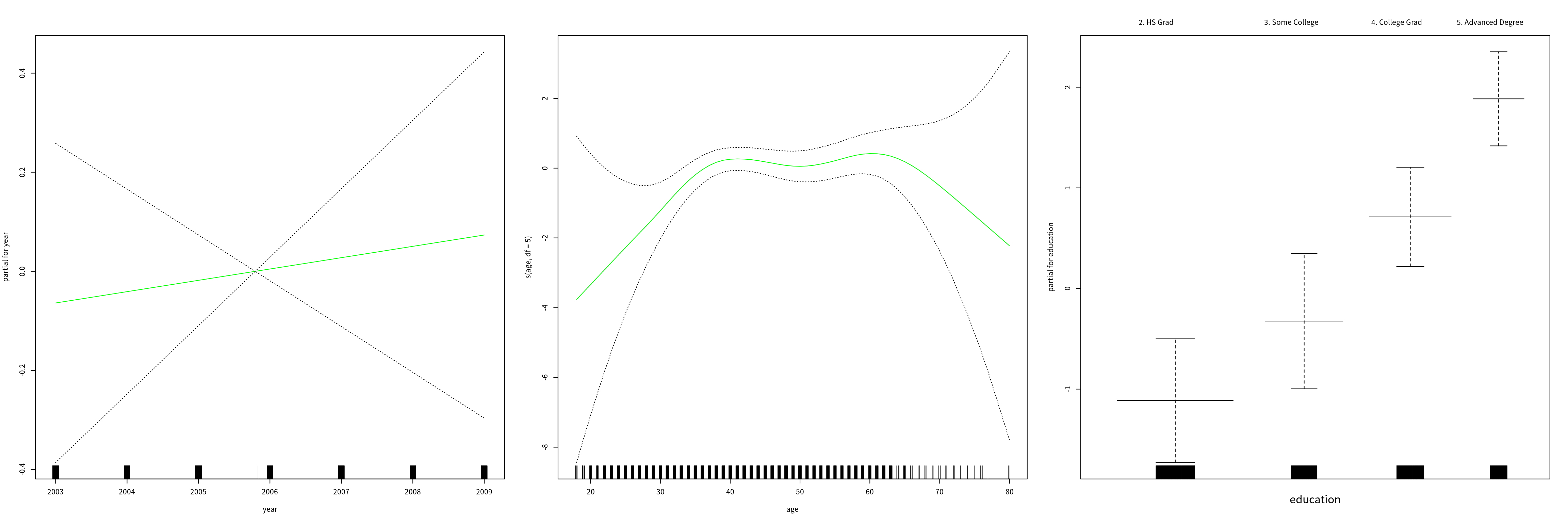

## 5. Advanced Degree 381 45因为我们可以排除这个类别并重现拟合得到更细节的结果,

gam.lr.s = gam(I(wage>250) ~ year + s(age, df = 5) + education, family = binomial,

data = Wage, subset = (education != "1. < HS Grad"))

par(mfrow = c(1, 3))

plot(gam.lr.s, se = T, col = "green")

Copyright © 2016-2021 weiya